Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The agentic AI enterprise platform market encompasses the software platforms, orchestration frameworks, infrastructure services, and application-layer tools that enable enterprises to build, deploy, and manage autonomous AI agents capable of multi-step reasoning, adaptive learning, and dynamic action execution. Unlike traditional generative AI systems that respond to single prompts, agentic AI platforms orchestrate workflows where multiple specialised agents collaborate—each with defined roles, tool access, memory systems, and decision-making capabilities—to accomplish complex business objectives without continuous human oversight.

The market has evolved through three distinct phases: the chatbot era (pre-2024), characterised by single-model conversational interfaces; the copilot era (2024–2025), where AI assistants augmented individual productivity within applications like Microsoft 365 Copilot and GitHub Copilot; and the current agentic era (2025 onward), where AI systems autonomously execute end-to-end business processes. Gartner predicts that 40% of enterprise applications will be integrated with task-specific AI agents by end of 2026, up from less than 5% in 2025. The shift is being described as the most significant enterprise AI transformation since the introduction of large language models.

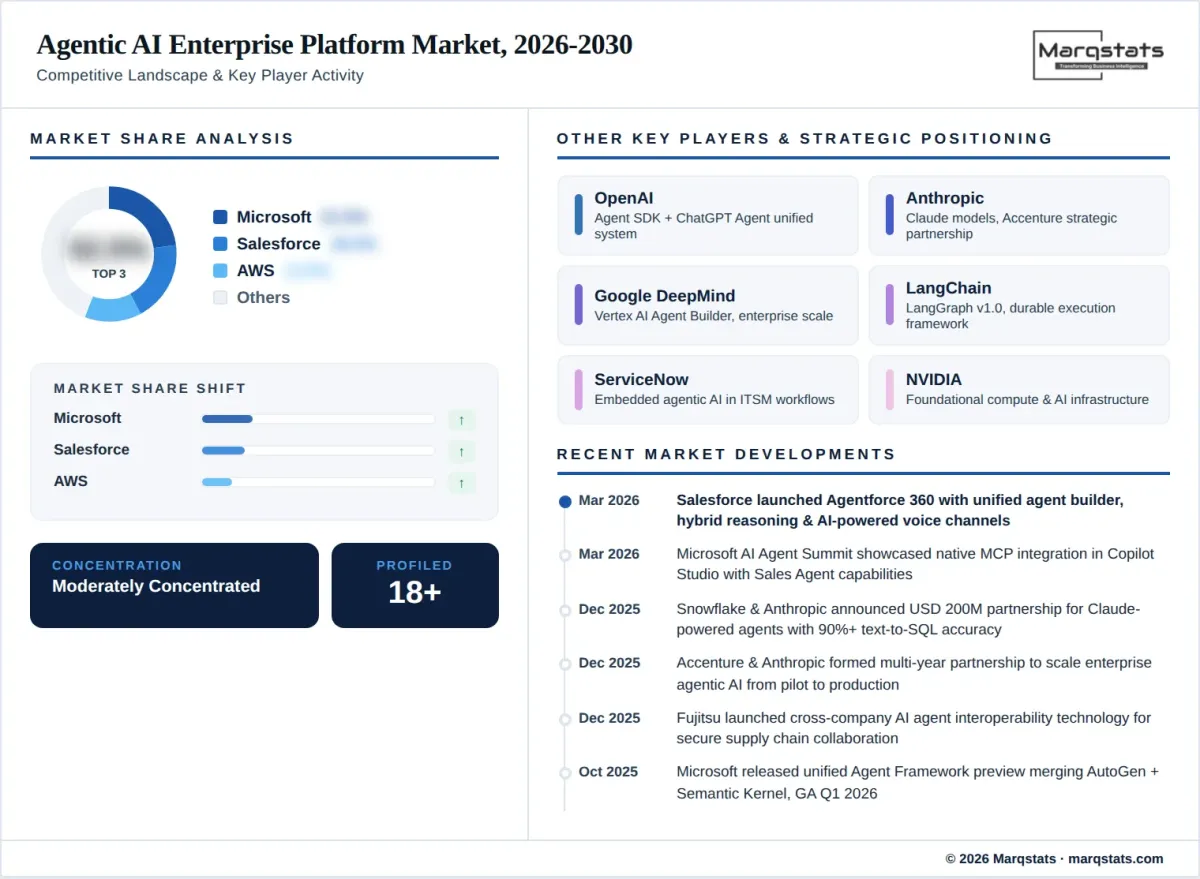

The market structure spans four vendor segments: Infrastructure and Framework Providers (NVIDIA, cloud hyperscalers) delivering foundational compute and orchestration tools; Platform Providers (OpenAI, Anthropic, LangChain) offering development environments for building custom agents; Agentic AI Services Providers (Accenture, KPMG, Capgemini) combining RPA with AI agent orchestration for turnkey automation; and Application Providers (Salesforce, Microsoft, ServiceNow) embedding agentic capabilities directly into end-user enterprise software. The competitive landscape is moderately concentrated, with the top five players holding just over half of revenue. Investment momentum remains exceptionally strong, with over USD 9.7 billion invested in agentic AI startups since 2023 and agentic AI funding reaching USD 2.8 billion in H1 2025 alone.

Market Dynamics

Key Drivers

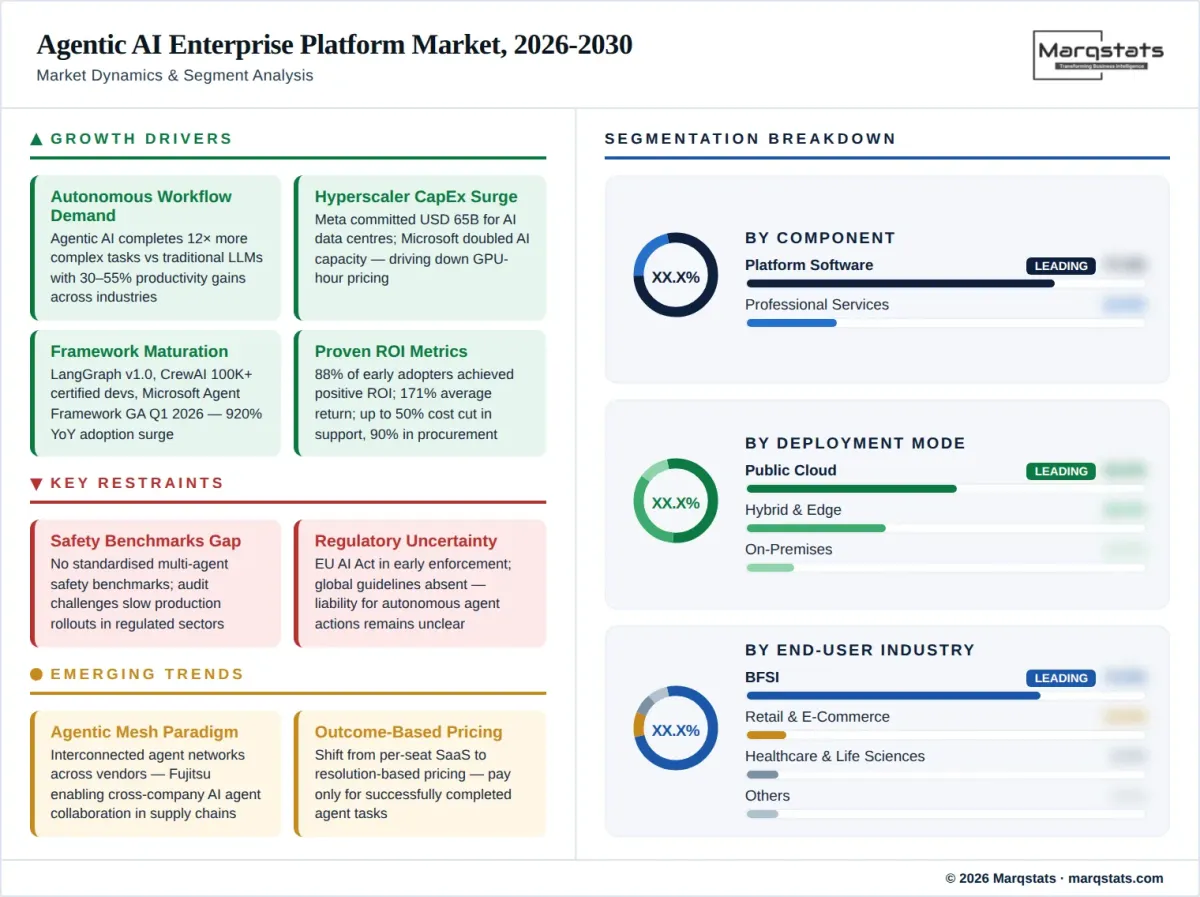

- Enterprise demand for autonomous workflow automation: Enterprises are moving beyond prompt-based AI assistance toward systems that can independently execute multi-step processes. Agentic AI has demonstrated the ability to complete up to 12 times more complex tasks compared to traditional LLMs, driven by dynamic feedback loops and autonomous decision-making. A Deloitte report found that AI-powered workflow automation delivers productivity enhancements of 30–55% across industries, while Salesforce’s Agentforce platform has been deployed by thousands of brands within its first quarter of availability.

- Hyperscaler capital expenditure lowering access barriers: Record infrastructure investment is democratising access to high-end GPU compute required for running agentic workloads. Meta earmarked USD 65 billion for AI data centres through 2025, Microsoft doubled AI capacity, and AWS expanded Bedrock agent services—collectively reducing GPU-hour pricing and enabling mid-market firms to run long-lived agents economically. The enterprise agentic AI development platform market linked to hybrid and edge deployments is forecast to expand from USD 3.3 billion in 2025 to USD 16.1 billion by 2030.

- Maturation of orchestration frameworks and developer tooling: Open-source frameworks have reached production readiness. LangGraph achieved v1.0 in late 2025 with durable execution and human-in-the-loop capabilities. CrewAI has certified over 100,000 developers through community courses. Microsoft merged AutoGen with Semantic Kernel into a unified Agent Framework (GA Q1 2026) with production SLAs. Developer adoption of agent frameworks surged 920% year-on-year, creating a deep ecosystem of reusable components and integrations.

- Compelling total cost of ownership and ROI metrics: Agentic AI delivers measurable financial returns. Customer support costs decrease by up to 50%, procurement operations by up to 90%. Early adopters project average ROI of 171% from deployments. 88% of early adopters achieved positive ROI according to a 2025 Google Cloud study. In software engineering, agentic AI enables 4x faster code debugging. These concrete metrics are accelerating C-suite approval for enterprise-wide deployment.

- Model Context Protocol (MCP) and interoperability standards: The emergence of open standards like MCP—enabling AI agents to access tools, context, and data from external systems—is reducing integration friction. Microsoft integrated MCP natively into Copilot Studio in 2025, while Salesforce’s Agentforce 3 added MCP support. This interoperability is creating an ecosystem where agents from different vendors can collaborate, dramatically expanding use case coverage.

Key Restraints

- Lack of standardised safety benchmarks: The absence of standardised multi-agent safety benchmarks raises compliance concerns and slows production rollouts, particularly in regulated sectors like financial services and healthcare. Enterprises deploying multiple autonomous agents face challenges in auditing agent decisions, preventing hallucinations, and ensuring governance consistency across hybrid cloud and edge environments.

- Regulatory uncertainty and compliance fragmentation: Governments and regulatory bodies are still developing AI governance frameworks. The EU AI Act introduces requirements for high-risk AI systems, but harmonised global guidelines remain absent. Uncertainty around legal liability for autonomous agent actions, data handling protocols, and ethical standards delays enterprise deployment in sectors like healthcare, financial services, and public administration.

- Talent scarcity and organisational readiness gaps: Building and managing multi-agent systems requires expertise in prompt engineering, graph-based workflow design, and human-AI collaboration that is scarce in the current labour market. By 2030, 39% of core skills will change, led by AI and cybersecurity capabilities. Many enterprises underestimate the organisational transformation required to move from pilot to production-scale agentic deployments.

- Vendor lock-in and portability concerns: Deep integration with specific cloud ecosystems (Azure for Microsoft Agent Framework, Salesforce Data Cloud for Agentforce) creates switching costs. While open-source frameworks like LangGraph offer portability, enterprise-grade features like production SLAs and compliance certifications often require commitment to a single vendor stack.

Key Trends

- Convergence of agent frameworks toward production readiness: The 2023–2024 explosion of agent frameworks has consolidated dramatically. Microsoft merged AutoGen and Semantic Kernel into a unified Agent Framework. LangChain publicly pivoted its developer community from chains to LangGraph for agent orchestration. CrewAI’s role-based model is becoming a standard for rapid prototyping. By 2026, the industry has moved from “which LLM is smartest?” to “which framework can manage 50 specialised agents without collapsing?”

- Consumption-based and outcome-based pricing models: The traditional per-seat SaaS pricing model is being disrupted. Salesforce Agentforce offers Flex Credits ($500 per 100,000 credits) alongside per-conversation and per-user licenses. Microsoft Copilot Studio uses credit capacity packs (25,000 credits for $200/month). Emerging players like Decagon are pioneering resolution-based pricing where enterprises pay only for successfully completed agent tasks—aligning vendor revenue with actual business outcomes.

- Rise of vertical and domain-specific agents: While horizontal platforms dominate current adoption, vertical AI agents specialised for specific industries are projected to grow at 62.7% CAGR through 2030. Causaly launched the first agentic AI platform specifically designed for life sciences R&D in September 2025. KPMG Velocity launched Global Business Services enabled by ServiceNow AI Platform to streamline finance, procurement, HR, and IT functions. Industry-specific compliance, terminology, and workflow patterns are driving this specialisation.

- Multi-agent orchestration and the ‘Agentic Mesh’ paradigm: The frontier of development is moving toward interconnected networks of specialised agents from different frameworks and vendors. A LangGraph ‘brain’ might orchestrate a CrewAI marketing team while calling OpenAI tools for sub-tasks. Fujitsu announced technology in December 2025 enabling AI agents from different companies to work together securely in supply chains. This interoperability-first approach is expected to define the market architecture by 2028.

Market Segmentation

Platform software leads the market with over 77% share in 2024, driven by integrated orchestration, safety tooling, and low-code agent builders. Major platforms include Salesforce Agentforce (with its Atlas Reasoning Engine for autonomous multi-step actions), Microsoft Copilot Studio (leveraging Power Platform and Azure AI), AWS Bedrock Agents, and Google Vertex AI Agent Builder. Platform software encompasses the development environments, runtime engines, monitoring dashboards, and governance tools required to build, test, deploy, and supervise AI agents at enterprise scale.

Professional services represent the fastest-growing component, as enterprises require consulting, implementation, and managed services to navigate the complexity of agentic AI adoption. Systems integrators like Accenture, which announced a multi-year strategic partnership with Anthropic in December 2025, are establishing dedicated agentic AI practice groups. Implementation timelines for enterprise platforms like Salesforce Agentforce and Microsoft Copilot can stretch to months, often necessitating external partners and specialised enterprise plans.

Public cloud retains approximately 53% market share due to hyperscaler convenience, broad service catalogues, and elastic compute for bursty agentic workloads. AWS Bedrock, Azure AI, and Google Cloud Vertex AI are the primary hosting environments. Cloud deployment enables rapid scaling of agent instances to handle demand spikes and provides access to the latest foundation models without on-premises hardware investment.

Hybrid and edge deployments are recording the fastest growth at 37.80% CAGR, driven by data sovereignty requirements, latency-critical use cases, and privacy-sensitive workloads. Enterprises host sensitive agent workflows on-premises while retaining cloud elasticity for non-sensitive interactions. AI PCs with dedicated neural processing units (NPUs) and edge servers like NVIDIA Jetson enable agents to operate offline, reducing inference costs and strengthening privacy compliance. The hybrid and edge segment is forecast to expand from USD 3.3 billion in 2025 to USD 16.1 billion by 2030.

Banking, financial services, and insurance leads enterprise agentic AI adoption, accounting for over 74% of the development platform market in 2024. Agents autonomously handle customer onboarding, claims processing, fraud detection, compliance workflows, and client advisory services. Multi-agent systems are being piloted by major institutions including ICBC and Ping An in China for cross-functional BFSI automation. Regulatory compliance requirements in financial services are driving demand for explainable, auditable agent architectures.

Retail and e-commerce is the fastest-growing vertical at a projected 39.05% CAGR through 2030. Agentic AI powers autonomous customer support, inventory management, personalised recommendations, dynamic pricing, and supply chain optimisation. Agents analyse real-time data, user behaviour, and browsing patterns to independently generate tailored promotions and provide proactive support interventions—delivering 4–7x conversion rate improvements in targeted processes.

Healthcare is a high-growth vertical with agents automating patient intake, clinical documentation, claims processing, and drug discovery workflows. Causaly’s agentic research platform, launched in September 2025, uses specialised AI agents to automate complex research workflows and deliver evidence-backed insights for pharmaceutical R&D. Integration with wearable devices and electronic health records is expanding agent utility across the care continuum.

By Geography

North America

North America dominates the agentic AI enterprise platform market with approximately 39% revenue share in 2025, anchored by the United States where the market was valued at USD 1.58 billion in 2024. The region benefits from the highest concentration of AI technology companies (OpenAI, Anthropic, Microsoft, Salesforce, Google), deep venture capital infrastructure (over USD 9.7 billion invested in agentic AI startups since 2023), and early enterprise adoption across financial services, technology, and professional services sectors. The US, Canada, Germany, France, China, India, and Japan are identified as the most attractive countries for agentic AI over the next five years.

Europe

Europe represents a significant growth market, driven by innovation ecosystems in the UK, Germany, and France, and amplified by regulatory catalysts like the EU AI Act and data sovereignty mandates. Three major technology companies committed approximately USD 17 billion in AI infrastructure investment in the UK in January 2025 alone (Vantage Data Centres, Nscale, and Kyndryl). European enterprises are prioritising sovereignty-compliant agentic solutions with on-premises and hybrid deployment models. The EU Cyber Resilience Act, requiring manufacturers to report product vulnerabilities by September 2026, is driving demand for compliant agentic AI platforms.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by India’s USD 1.2 billion AI Mission, enterprise-scale deployments in BFSI and telecom, and cloud infrastructure expansion. Over 80% of Indian organisations are actively exploring autonomous agent development according to Deloitte. China’s major financial institutions (ICBC, Ping An) are piloting multi-agent systems for BFSI automation. Southeast Asian technology companies including Grab and DBS are deploying agentic copilots for customer experience and productivity. The region’s combination of large-scale digital transformation programmes, government AI investments, and rapidly growing developer ecosystems positions it for outsized growth through 2030.

Rest of World

Latin America, the Middle East, and Africa represent emerging frontiers for agentic AI enterprise platforms, with adoption concentrated in Brazil, the UAE, and South Africa. Enterprise adoption in these regions is primarily driven by multinational corporations deploying global agentic AI platforms and by government-led digital transformation programmes. The relatively nascent but growing cloud infrastructure in these regions is expected to support accelerating adoption in the 2028–2030 timeframe as hyperscalers expand their regional data centre footprints.

How Competition Is Evolving

The agentic AI enterprise platform market features a dynamic competitive landscape spanning four distinct vendor categories. Infrastructure and Framework Providers like NVIDIA, AWS, and Google deliver the foundational compute and AI services. Platform Providers including OpenAI, Anthropic, and LangChain offer development environments for building custom agents. Agentic AI Services Providers such as Accenture, Capgemini, and KPMG combine consulting with implementation. Application Providers like Salesforce, Microsoft, and ServiceNow embed agentic capabilities into enterprise software. The market is moderately concentrated, with the top five players holding just over half of total revenue.

Salesforce and Microsoft are waging a high-profile battle for enterprise agentic AI supremacy. Salesforce’s Agentforce platform (renamed from Einstein Copilot in January 2025) is CRM-native, offering autonomous agents for sales, service, marketing, and commerce built on the Atlas Reasoning Engine. Pricing spans Agentforce Add-ons at $125 per user/month to Agentforce 1 Editions at $550 per user/month. Microsoft’s strategy centres on embedding agents within its ubiquitous Microsoft 365 and Dynamics 365 ecosystem, with Copilot Studio enabling low-code agent creation and over 160,000 organisations having created more than 400,000 custom agents in just three months. The October 2025 merger of AutoGen and Semantic Kernel into a unified Microsoft Agent Framework (GA Q1 2026) signals Microsoft’s commitment to production-grade enterprise agentic infrastructure.

On the open-source and developer tooling front, LangGraph (v1.0 in late 2025) has emerged as the framework of choice for enterprises requiring precise state management and durable execution in complex workflows. CrewAI dominates rapid prototyping with its intuitive role-based model and over 100,000 certified developers. OpenAI’s Agent SDK and the July 2025 launch of ChatGPT Agent (integrating Operator and Deep Research into a unified agentic system) position OpenAI as both a model provider and agent platform. New entrants including NTT DATA (Smart AI Agent Ecosystem, May 2025) and Snowflake (partnership with Anthropic for Claude-powered agents, December 2025) are expanding the ecosystem rapidly.

Companies Covered

The report profiles 18++ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the global agentic AI enterprise platform market covering the period 2021–2030, with 2025 as the base year, historical data from 2021 to 2025, and forecast projections from 2026 to 2030. The study examines market size in USD billion, growth trends, competitive landscape, and segment-level forecasts by component (platform software, professional services), deployment mode (public cloud, hybrid and edge, on-premises), agent type (ready-to-deploy, build-your-own), end-user industry (BFSI, retail and e-commerce, healthcare, technology and software, professional services, others), and region.

The analysis covers the complete vendor ecosystem from infrastructure providers and orchestration framework developers through platform builders, systems integrators, and enterprise application providers with embedded agentic capabilities. Competitive profiling spans 18 companies across all four vendor categories. The report provides strategic guidance on framework selection, deployment architecture, ROI benchmarking, and organisational readiness assessment for enterprise agentic AI adoption.