Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The global capability centre IT services market encompasses the captive, in-house technology service delivery operations established by multinational enterprises in offshore and nearshore locations. Unlike traditional IT outsourcing, where services are delivered by third-party vendors (such as Infosys, TCS, or Wipro), GCCs are fully owned and operated by the parent company, providing 100% control over talent, intellectual property, data security, and strategic direction. The market scope covers IT infrastructure services, application development and modernisation, cloud migration and management, AI/ML engineering and data analytics, cybersecurity and DevSecOps, enterprise platform services (ERP, CRM), quality engineering, and digital product development. The study period spans 2021–2030, with 2025 as the base year.

The GCC model has undergone a profound transformation over the past decade. What began in the late 1990s as cost-centric offshore units for basic IT and back-office services has evolved into strategic hubs driving global innovation. India’s GCC revenue grew from USD 19.60 billion in FY2014–15 to USD 64.60 billion in FY2024, reflecting an 11.4% annual growth rate. As of December 2025, 52% of Procore’s workforce and an equivalent proportion of major tech companies’ global headcounts are based in Indian GCCs. Engineering Research & Development (ER&D) accounts for approximately 56% of overall GCC revenue, with digital engineering projected to grow at approximately 20% CAGR. Global leadership roles based in Indian GCCs have grown at approximately 40% CAGR over five years, reaching 6,500+ roles in 2024 (including 1,050+ women leaders), with projections surpassing 30,000 by 2030.

The broader capability centre services market was valued at USD 172.34 billion in 2024 and is forecast to reach USD 403.22 billion by 2032, expanding at 11.21% CAGR. Within this, IT services is the largest and fastest-growing segment, driven by the shift toward hybrid cloud architectures, Site Reliability Engineering (SRE), DevSecOps, AI-native operations, and enterprise-wide digital transformation. The structural trend from outsourcing to captive models is accelerating: enterprises that build future-ready GCCs powered by AI, automation, and domain-led expertise are unlocking competitive advantage, operational savings of 30–60% versus equivalent US/European operations, and long-term innovation capability with full IP ownership.

Market Dynamics

Key Drivers

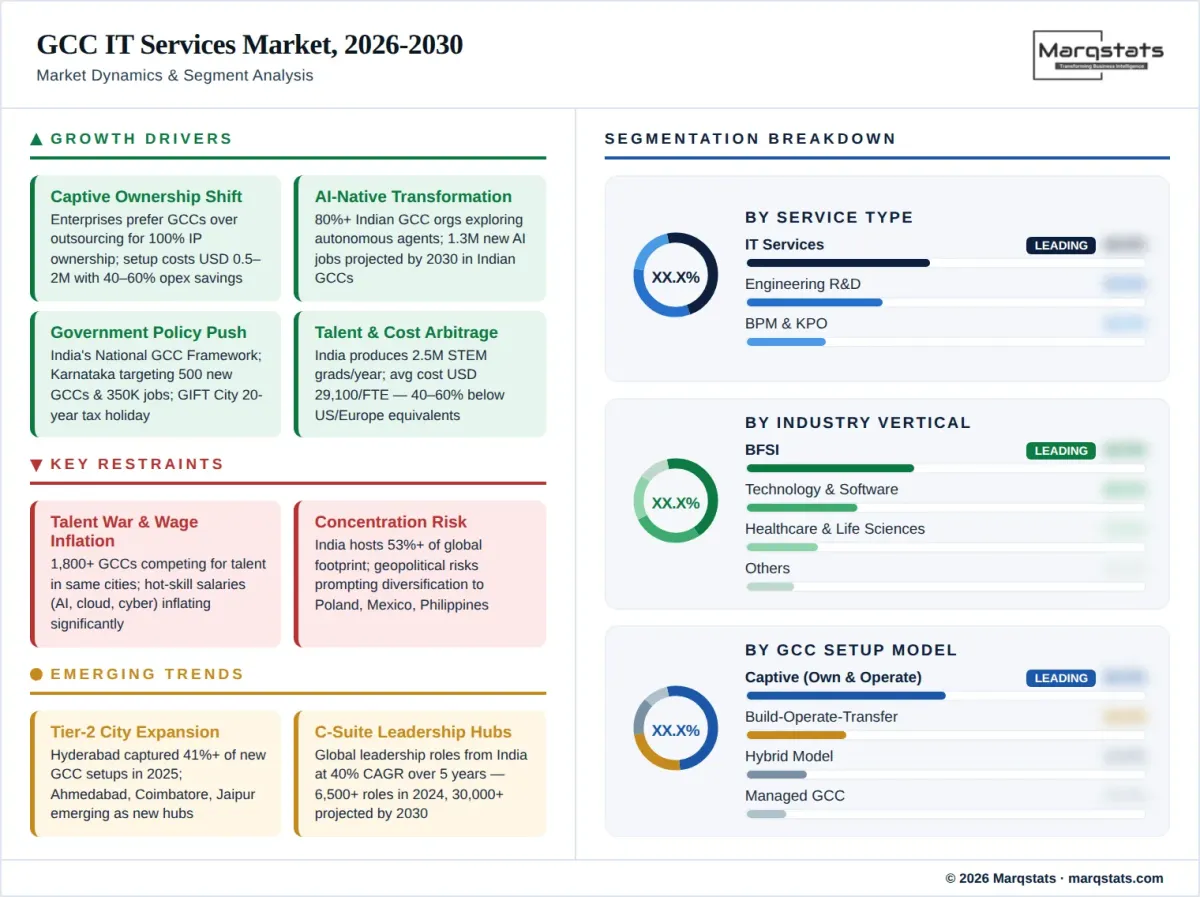

- Strategic shift from outsourcing to captive technology ownership: Enterprises are increasingly preferring GCCs over third-party outsourcing to retain control over intellectual property, data security, and strategic innovation. The captive model provides 100% IP ownership, cultural alignment with the parent organisation, and the ability to build deep domain expertise. GCC setup costs are modest—a 50–100 person centre costs USD 500,000 to USD 2 million, with annual operating costs 40–60% lower than US or European equivalents.

- AI-native transformation and generative AI adoption: Over 80% of Indian GCC organisations are actively exploring autonomous agent development. GCCs are becoming the primary engines for enterprise AI engineering, including LLM fine-tuning, MLOps, agentic AI orchestration, and AI-powered cybersecurity. India’s GCC workforce is projected to create 1.3 million new AI-related jobs by 2030. Companies are building dedicated AI Centres of Excellence within their GCCs—Infosys and Google Cloud opened a joint AI Innovation Center in Bangalore in November 2025.

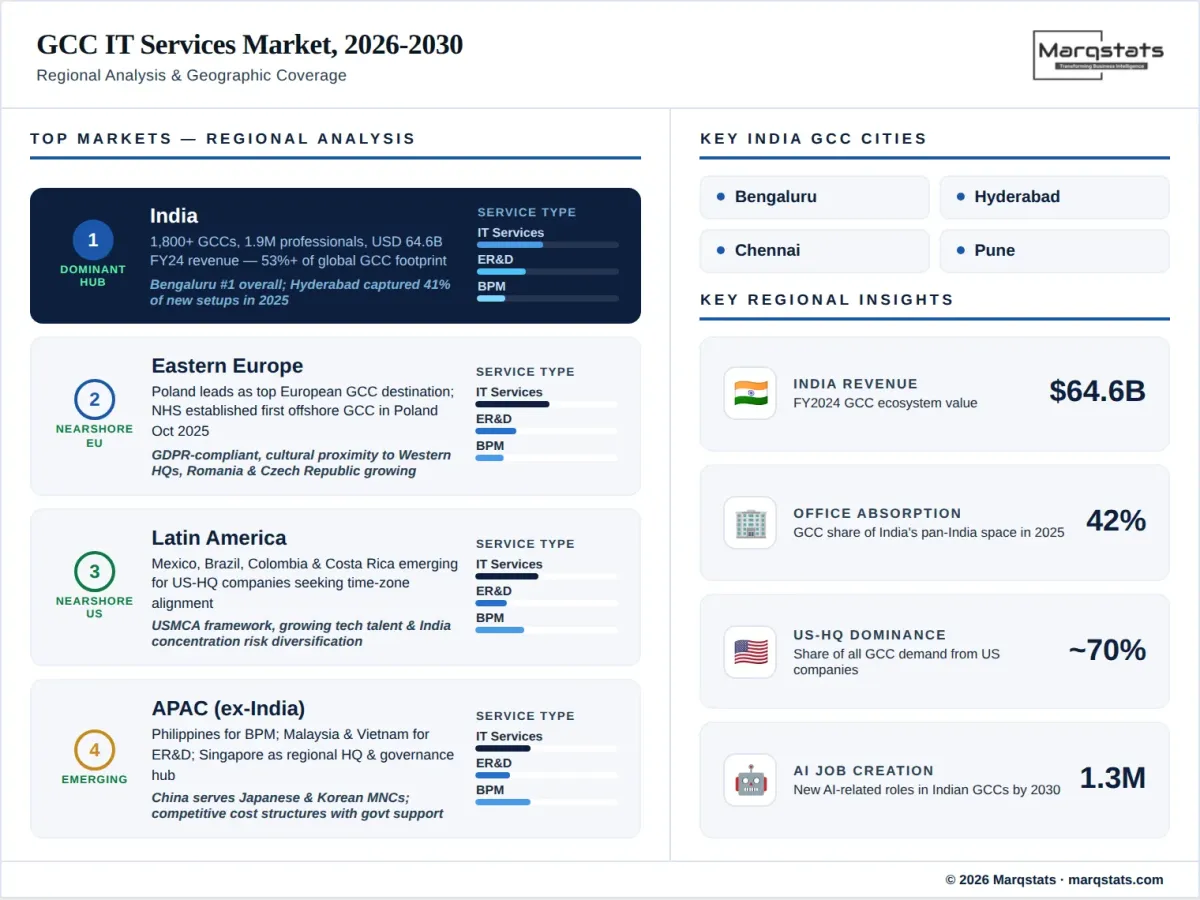

- Government policy support and investment incentives: India’s Union Budget 2025–26 announced a National Framework for GCCs to promote expansion into Tier-2 cities. The budget set a uniform 15.5% safe harbour margin for transfer pricing (raised threshold from INR 300 crore to INR 2,000 crore), covering over 1,000 existing GCCs. GIFT City’s tax holiday was extended to 20 years. Karnataka launched India’s first dedicated GCC policy in November 2024, targeting 500 new GCCs and 350,000 jobs by 2029 with rental reimbursements, EPF support, and 45-day fast-track approvals. Rajasthan unveiled its GCC Policy-2025 to create 1.5 lakh jobs across 200+ centres.

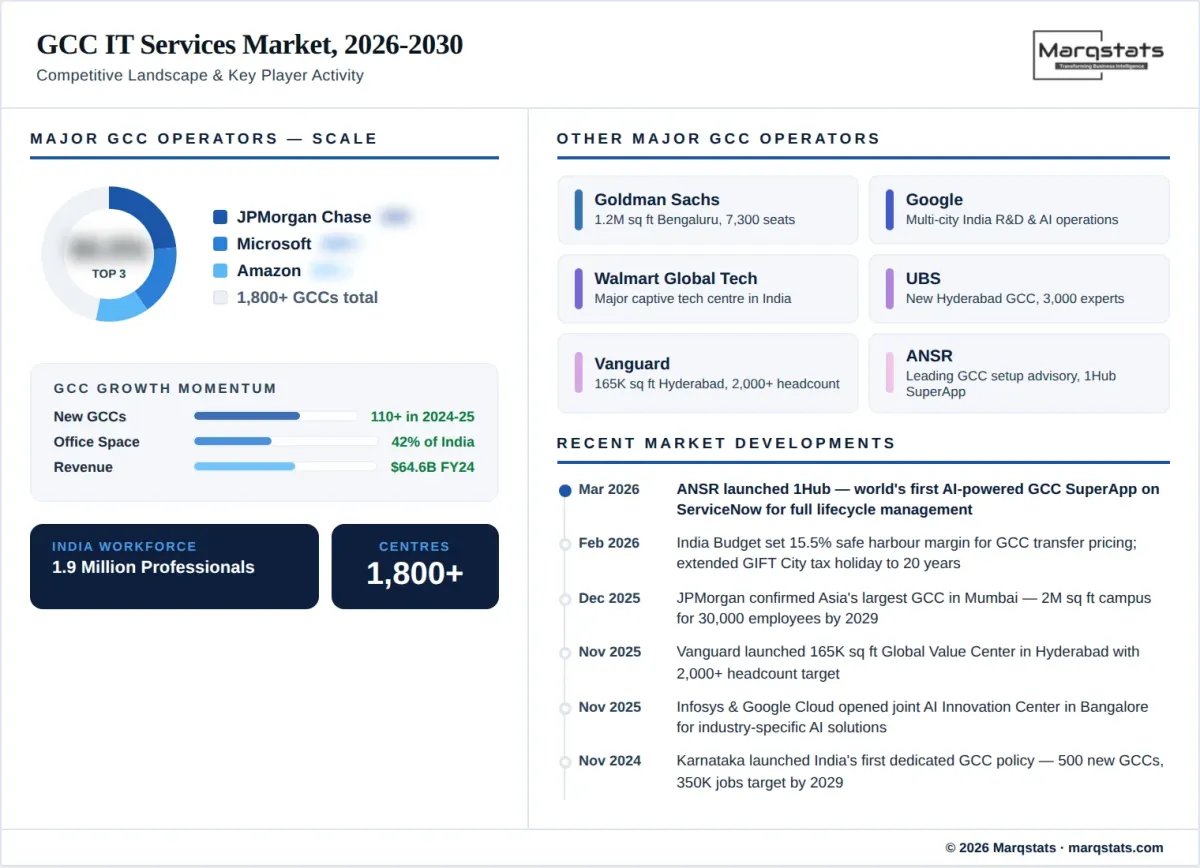

- Massive infrastructure investment by global enterprises: JPMorgan Chase is building Asia’s largest GCC in Mumbai (2 million sq ft, 30,000 employees, completion 2029). Vanguard launched a 165,000 sq ft Global Value Center in Hyderabad (2,000+ headcount). UBS inaugurated a GCC in Hyderabad deploying 3,000 experts. GCCs accounted for 42% of pan-Indian office space absorption in the first nine months of 2025, with full-year absorption expected to reach a record 75 million square feet.

- Talent scale and cost arbitrage: India produces 2.5 million STEM graduates annually. The cost per full-time equivalent in Indian GCCs averages USD 29,100 (projected to reach USD 37,760 by 2030), delivering 40–60% cost savings versus US/European operations while providing access to world-class engineering, data science, and AI talent at scale.

Key Restraints

- Talent competition and wage inflation: With over 1,800 GCCs competing for talent in the same Indian cities, salary inflation in hot-skill areas (AI/ML, cloud architecture, cybersecurity) is significant. Attrition rates remain elevated in Tier-1 cities, pushing companies toward Tier-2 locations and intensifying competition for senior leadership talent.

- Infrastructure constraints in Tier-1 cities: Urban congestion, limited office space availability, and rising commercial real estate costs in Bengaluru, Hyderabad, and Mumbai are approaching saturation. While Tier-2 expansion addresses this, newer cities lack the ecosystem maturity and infrastructure depth of established hubs.

- Data sovereignty and regulatory complexity: Multinational enterprises face complex cross-border data transfer regulations, particularly from the EU (GDPR), the US, and India’s Digital Personal Data Protection Act 2023. Ensuring compliance across multiple jurisdictions while maintaining operational efficiency requires sophisticated governance frameworks.

- Geopolitical risk and concentration risk: India’s dominance (53%+ of global GCC footprint) creates concentration risk for multinational enterprises. Trade tensions, visa policy changes, and geopolitical uncertainties prompt some enterprises to diversify GCC footprints across Poland, Mexico, Philippines, and Latin America as risk mitigation strategies.

Key Trends

- Tier-2 city expansion reshaping the geographic landscape: Hyderabad captured over 41% of all new GCC setups in India between January and November 2025, surpassing Bengaluru. Emerging hubs like Ahmedabad, Coimbatore, Bhubaneswar, Jaipur, and Kochi are attracting new centres with lower operating costs, untapped talent pools, and state government incentives. Projections suggest a significant share of new GCCs by 2030 will emerge from previously untapped cities.

- Rise of mid-market and first-time GCC adopters: 35% of mid-market GCCs in India were set up in just two years (2023–2025). Companies that previously relied entirely on outsourcing are establishing their first captive centres, attracted by Build-Operate-Transfer (BOT) models that reduce setup risk. GCC-as-a-service providers like ANSR, Zinnov, and Inductus are enabling rapid setup in 3–6 months.

- From execution hubs to C-suite leadership centres: Indian GCCs are evolving from execution-focused operations to strategic leadership centres. Global leadership roles from India have grown at 40% CAGR over five years. Nearly two-thirds of Mega GCC heads now come from technical backgrounds, many managing dual mandates across India operations and global portfolios. 88 Mega GCCs (employing 50% of total GCC workforce) are projected to grow to 230+ by 2030.

- GCC-startup collaboration ecosystems: GCCs are increasingly partnering with Indian startups for innovation in AI, cybersecurity, IoT, and digital engineering. This collaboration model allows multinational enterprises to access cutting-edge technology developed by India’s vibrant startup ecosystem while startups gain enterprise-scale deployment opportunities and revenue. The GCC-startup nexus is being described as India’s growth powerhouse for 2026.

Market Segmentation

IT services dominate the GCC landscape with approximately 46% of global revenue (USD 79.25 billion in 2024). This segment includes cloud migration and multi-cloud management, application modernisation, cybersecurity operations (SOC-as-a-service), AI/ML engineering and data platforms, DevSecOps, infrastructure services, and enterprise platform management (SAP, Salesforce, ServiceNow). The shift toward hybrid cloud, SRE practices, and AI-native operations continues to strengthen IT services as the largest and fastest-growing GCC function.

ER&D accounts for approximately 56% of Indian GCC revenue and is projected to grow at approximately 20% CAGR. GCCs are the primary engines for product engineering, automotive software development, semiconductor design, IoT platform development, and digital twin implementation. Texas Instruments opened an advanced semiconductor R&D centre in Bengaluru, while companies like Mercedes-Benz Tech, BMW, and Bosch run major ER&D centres in Pune and Bengaluru. This segment represents the highest-value function within GCCs, directly contributing to parent companies’ product roadmaps and patent portfolios.

BPM and KPO functions represent approximately one-third of GCC workforce deployment, covering finance and accounting, HR services, procurement, compliance, and analytics. These functions have evolved significantly from transactional processing to judgment-intensive knowledge work, with AI-powered automation (RPA, intelligent document processing, workflow orchestration) driving hyper-automation across processes. KPMG Velocity launched Global Business Services enabled by ServiceNow AI Platform to streamline finance, procurement, HR, and IT functions.

BFSI is the largest vertical for GCC IT services, driven by the concentration of global banks’ technology operations in India. JPMorgan Chase’s multicity operations account for approximately 55,000 employees. Goldman Sachs’ Bengaluru office spans 1.2 million square feet with 7,300 seats. UBS inaugurated a GCC in Hyderabad deploying 3,000 experts. Hyderabad now hosts all seven of the world’s top asset management companies by AUM. BFSI GCCs handle AI-driven risk analytics, cybersecurity, digital banking platforms, fintech innovation, and regulatory compliance.

Technology companies operate some of the largest and most mature GCCs globally. Microsoft’s India Development Center in Hyderabad is one of its largest global R&D hubs. Amazon’s Hyderabad campus covers 9.7 acres with 15,000 employees. Google, Walmart Global Tech, and Cisco run major operations across multiple Indian cities. These GCCs handle product engineering, cloud infrastructure development, AI research, and platform innovation at scale.

Healthcare and pharma GCCs are a fast-growing segment, driven by clinical data analytics, drug discovery support, and regulatory compliance. Eli Lilly, Agilent, and Sanofi have expanded or launched GCCs in Hyderabad. The UK’s NHS established its first dedicated offshore GCC in Poland for healthcare data analytics in October 2025. GCCs in this vertical are increasingly focused on AI-powered diagnostics, clinical trial optimisation, and pharmacovigilance.

By Geography

India

India is the undisputed global hub for GCCs, hosting over 1,800 centres (53%+ of global footprint) employing 1.9 million professionals with USD 64.6 billion in FY2024 revenue. Bengaluru remains the overall leader, but Hyderabad captured 41–46% of all new GCC setups in January–November 2025 (approximately 41 new centres), surpassing Bengaluru (21–33 new centres). Chennai, Pune, Mumbai, and NCR are other major hubs. The ecosystem is projected to reach 2,100–2,400 centres by 2030, employing 2.5–2.8 million professionals. US-headquartered firms account for approximately 65–70% of the GCC footprint, followed by European firms at 35%. GCCs contributed to 42% of India’s pan-India office space absorption in 2025.

Eastern Europe

Poland is the leading European GCC destination, hosting major centres for financial services, healthcare, and technology companies. The UK’s NHS established its first offshore GCC in Poland in October 2025 for healthcare data analytics. Romania, Czech Republic, and Hungary also serve as nearshore GCC locations for European headquarters, offering proximity, regulatory alignment, and EU data protection compliance. Eastern European GCCs are particularly favoured by companies seeking GDPR-compliant operations with cultural proximity to Western European headquarters.

Latin America

Mexico, Brazil, Colombia, and Costa Rica are emerging as nearshore GCC destinations for US-headquartered companies seeking geographic diversification and time-zone alignment. Mexico’s proximity to the US, growing technology talent pool, and USMCA trade framework make it particularly attractive for GCC establishment. Latin American GCCs focus on application development, customer operations, and digital marketing services, with the region growing as enterprises seek to reduce concentration risk from India-heavy GCC portfolios.

Asia-Pacific (ex-India)

The Philippines remains a major BPM and customer operations hub, though its GCC footprint tilts more toward voice-based services than IT engineering. China’s GCC ecosystem serves primarily Japanese and Korean multinationals. Malaysia and Vietnam are emerging destinations for ER&D and technology GCCs with competitive cost structures and government support. Singapore functions as a regional headquarters and governance hub for GCC operations across Southeast Asia, rather than a large-scale delivery centre.

How Competition Is Evolving

The GCC IT services market features a distinctive competitive structure. Unlike traditional software or services markets, the primary ‘competitors’ are not vendors but the enterprises themselves—multinational corporations that build and operate their own captive centres. The competitive dynamics exist between GCC setup advisory firms, managed GCC service providers, and the underlying IT outsourcing companies whose business models are being disrupted by the captive GCC trend. Key GCC advisory and setup firms include ANSR (which launched 1Hub, the world’s first AI-powered GCC SuperApp in 2025), Zinnov, EY, Deloitte, PwC, and KPMG. IT services firms like Infosys, TCS, Wipro, and HCLTech are adapting by offering GCC strategy and transformation consulting, with HCLTech earning dual leadership in Everest Group’s 2025 PEAK Matrix for GCC Strategy and Transformation.

Among enterprise GCC operators, the BFSI sector leads in scale. JPMorgan Chase is the largest, with approximately 55,000 India-based employees and Asia’s largest GCC under construction in Mumbai. Goldman Sachs, Citibank, HSBC, American Express, Deutsche Bank, Standard Chartered, UBS, and Vanguard all operate major GCCs. In technology, Microsoft, Amazon, Google, Walmart, Cisco, and Oracle run massive captive operations. Industrial and automotive GCCs include Mercedes-Benz Tech, BMW, Bosch, Siemens, and Rolls-Royce. Recent high-profile new entrants include Costco (Hyderabad), Netflix (HITEC City creative-tech hub), Southwest Airlines (Hyderabad), Charles Schwab (Hyderabad), and Sanofi (Hyderabad expansion).

The competitive dynamics are also shifting geographically. Hyderabad is emerging as the fastest-growing GCC city globally, supported by Telangana’s proactive policy framework that successfully anchored over 70 GCCs in 2024–2025 alone. Karnataka, Maharashtra, and Rajasthan are intensifying inter-state competition through dedicated GCC policies, infrastructure investments, and talent development programmes. Real estate developers like Embassy REIT, Brookfield, and Mindspace are building dedicated GCC parks to meet surging demand.

Companies Covered

The report profiles 18++ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the global capability centre IT services market covering the period 2021–2030, with 2025 as the base year, historical data from 2021 to 2025, and forecast projections from 2026 to 2030. The study examines market size in USD billion, growth trends, competitive landscape, and segment-level forecasts by service type (IT services, ER&D, BPM/KPO), GCC setup model (captive, BOT, hybrid, managed), industry vertical (BFSI, technology, healthcare, retail, manufacturing), GCC maturity stage (execution, portfolio, transformation), and geography (India, Eastern Europe, Latin America, APAC).

The analysis covers the complete GCC ecosystem from enterprise GCC operators and advisory/setup firms through real estate infrastructure providers and talent development platforms. Competitive profiling spans 18 entities including major GCC operators and advisory firms. The report provides strategic guidance on GCC location selection, setup model evaluation, AI integration roadmaps, and cost-benefit benchmarking for enterprises evaluating captive centre establishment or expansion.