Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The India EV battery swapping market encompasses the infrastructure, services, and technology ecosystem enabling electric vehicle users to exchange depleted battery packs for fully charged ones at dedicated swap stations rather than relying on plug-in charging. The market covers hardware (swap stations, battery management systems, IoT-enabled battery packs), software (fleet management platforms, mobile applications, real-time monitoring), and services (BaaS subscriptions, pay-per-use transactions, franchise operations) across two-wheeler, three-wheeler, and emerging heavy commercial vehicle segments.

India's battery swapping landscape has evolved from a nascent, startup-driven grey zone into a formalised component of the national EV infrastructure stack. The January 2025 Ministry of Power guidelines explicitly recognised battery swapping and charging stations within the regulatory framework, while NITI Aayog's February 2026 transport report described swapping as a key BaaS enabler for 2W/3W mobility and confirmed that interoperability standards are being pursued through BIS. The installed footprint has expanded sharply, with approximately 2,500–2,600 operational kiosks as of early 2026, concentrated in high-utilisation commercial corridors across metropolitan India. For broader electric three-wheeler market dynamics, including the e-rickshaw segment that forms a core swapping use case, see the India Electric Three-Wheeler Market report on Marqstats.

The market's current centre of gravity remains commercial two-wheelers and three-wheelers, especially delivery fleets, e-rickshaws, and ride-hailing vehicles where high daily utilisation (175–200 km) makes rapid refuelling economics compelling. However, the ecosystem is broadening across four vectors: policy formalisation through central and state guidelines, public-node deployment at metro and railway stations, franchise and fuel-retail scaling models, and early heavy-duty adoption in port logistics. This trajectory positions battery swapping as a structurally important enabler of India's electric mobility transition, particularly for commercial and shared transport segments.

Market Dynamics

Key Drivers

- Government policy formalisation and capital subsidies — The PM E-DRIVE scheme's INR 2,000 crore allocation for EV charging infrastructure including battery swapping stations, with up to 80% capital subsidy on upstream infrastructure at any location and up to 100% subsidy at government premises, has dramatically improved the investment case for swapping operators. The Ministry of Power's January 2025 battery swapping guidelines further mandated state utilities to supply power connections within predefined timelines, removing a critical permitting bottleneck.

- Explosive growth in last-mile delivery and gig economy — India's quick-commerce sector and food-delivery platforms have created sustained, high-volume demand for electric two-wheeler fleets requiring near-zero downtime. Battery swapping's two-to-three-minute turnaround enables delivery riders to complete more orders per day, directly improving daily earnings. Companies like Zypp, Shadowfax, Rapido, and Loadshare now actively integrate swappable-battery EVs into their delivery networks.

- BaaS model reducing EV upfront costs by 30–40% — By decoupling battery ownership from the vehicle, BaaS arrangements bring the upfront cost of an electric two-wheeler or three-wheeler significantly closer to ICE equivalents. Since batteries represent 30–50% of EV cost, this pricing innovation unlocks adoption among price-sensitive commercial operators and individual buyers who otherwise could not afford full-battery EVs.

- OEM validation through mainstream product launches — Honda Motor's entry into Indian battery swapping through its e:Swap service and the Activa e: scooter, supported by 500 planned swap stations across Bengaluru, Delhi, and Mumbai by March 2026, has validated swapping as a mainstream refuelling architecture for mass-market OEMs. This signals a shift from swapping being perceived as a startup-only model to an OEM-endorsed infrastructure standard.

- Rising electric three-wheeler registrations — India's e-rickshaw fleet has expanded rapidly across urban and semi-urban markets, with three-wheelers commanding approximately 55% of battery swap utilisation. Government mandates encouraging clean last-mile public transport and cargo movement create a self-reinforcing cycle of vehicle electrification and swapping infrastructure deployment. For deeper coverage of this segment, see the India Electric Three-Wheeler Market report on Marqstats.

Key Restraints

- Absence of unified interoperability standards — OEMs continue to use proprietary battery designs, limiting cross-platform compatibility at swap stations. While BIS-led standardisation efforts are underway, no binding national standard for swappable battery packs currently exists. This fragmentation forces operators to maintain multiple battery inventories and reduces station utilisation efficiency.

- High capital expenditure for station buildout and battery inventory — Each swap station requires investment of INR 10–40 lakh depending on format, plus substantial working capital for battery inventory. Maintaining fully charged battery banks at each station creates capital-intensive operations, particularly in cities with uneven demand density.

- Grid infrastructure limitations in emerging cities — Many Tier-2 and Tier-3 cities lack the electrical infrastructure needed to support dense swap station networks, each of which requires reliable power connections for continuous battery charging. Transformer upgrades, power connection approvals, and inconsistent electricity supply pose real constraints to geographic expansion beyond established metropolitan corridors.

- Consumer trust and safety perceptions — Shared-use battery packs raise concerns about battery degradation, safety, and reliability among some users. High-profile lithium-ion battery fire incidents in India's EV sector have heightened safety scrutiny, and the absence of comprehensive national testing standards until recently (SUN Mobility's AIS-038 certification in March 2026 was the first such milestone for heavy-duty platforms) has contributed to caution.

Key Trends

- Deployment at public transport nodes — Battery swapping stations are increasingly being deployed at metro stations, railway stations, bus depots, and fuel-retail outlets. In early 2026, Indofast Energy partnered with Mumbai Metro Rail Corporation to deploy 23 swap stations across 8 stations on the Aqua Line 3 corridor, while Battery Smart licensed a station at Banaras Railway Station. These high-footfall locations improve utilisation rates and reduce land-acquisition friction.

- Franchise and asset-light scaling models — Operators are shifting toward franchise-based expansion to accelerate coverage. Indofast Energy launched a franchise programme in December 2025 offering entrepreneurs the ability to set up swap stations with INR 10–40 lakh investment and projected annual returns of up to 30%. This model reduces the capital burden on primary operators while enabling rapid Tier-2 and Tier-3 city penetration.

- Heavy commercial vehicle swapping moving from pilot to production — The September 2025 launch of India's first fleet of 50 battery-swappable heavy-duty electric trucks at JNPA's Nhava Sheva terminal, and SUN Mobility's March 2026 AIS-038 certification for high-voltage swappable battery platforms for trucks and buses, represent structural shifts in the addressable market beyond light vehicles.

- Integration of IoT, predictive analytics, and smart batteries — Next-generation swap stations incorporate IoT-enabled batteries with real-time monitoring of charge cycles, temperature, and state-of-health (SoH). Battery Smart's technology stack uses predictive maintenance to minimise downtime, while Yuma Energy's January 2025 next-gen battery is designed for interoperability across multiple 2W/3W OEM platforms.

Market Segmentation

The three-wheeler segment dominated the India EV battery swapping market in 2025, accounting for approximately 55% of total swap activity. Electric rickshaws (e-rickshaws) represent the single largest use case, with their high daily utilisation of 150–200 km, fixed urban routes, and cost-sensitive owner-operators making battery swapping's pay-per-use economics highly compelling. Battery swapping eliminates the four-to-six-hour charging downtime that directly impacts driver earnings in the gig and public transport economy. The segment also includes cargo three-wheelers used in intra-city logistics and e-commerce last-mile delivery.

The two-wheeler segment is the fastest-growing category, projected to expand at a CAGR of approximately 25.3% during the forecast period. Growth is driven by favourable government subsidies, strict emission standards, and the expansion of delivery fleets for platforms such as Swiggy, Zomato, and Amazon. Honda's entry with the Activa e: swap-only scooter, Bounce Infinity's subscription-based scooter swapping, and Ola Electric's swap-ready patent filings for B2B scooters all signal deepening OEM engagement. The lighter battery packs (10–12 kg) used in two-wheelers facilitate rapid manual swaps, enabling station formats as compact as 250 square feet.

Although still at an early stage, heavy-duty battery swapping has moved from concept to operational deployment. The September 2025 launch of 50 battery-swappable heavy trucks at Jawaharlal Nehru Port Authority and SUN Mobility's AIS-038-certified high-voltage swappable platform (50 kWh and 100 kWh variants at 660V) have established commercial proof points. SUN Mobility and Veera Vahana also unveiled India's first 10.5-metre battery-swappable intercity bus at Prawaas 4.0 in August 2024. This segment represents the next frontier of market expansion, particularly for port logistics, intercity buses, and freight corridors.

Pay-per-use is the dominant service model, accounting for the majority of swap transactions. This model appeals to individual riders, delivery executives, and small fleet operators who prioritise financial flexibility and operational agility. Users pay based on actual swap instances without long-term commitments or large upfront investments. The model's accessibility has made it particularly effective in driving adoption among price-sensitive demographics, including e-rickshaw drivers and gig-economy delivery partners.

The subscription model is gaining traction, particularly among fleet operators, bus transit agencies, and large logistics companies with predictable daily routes and stable utilisation patterns. Electric buses with fixed routes benefit from subscription arrangements that provide guaranteed swap availability and predictable energy costs. Subscription models also facilitate better fleet-level cost planning and typically include service-level guarantees on battery health and swap turnaround times.

Lithium-ion batteries dominate the India EV battery swapping market and are rapidly gaining further share. Their superior energy density, longer cycle life, lighter weight, and declining costs make them the preferred choice for both 2W/3W and emerging heavy-vehicle applications. The global trend toward lower lithium-ion cell costs, exemplified by breakthroughs pushing costs below USD 56/kWh for LFP chemistries, strengthens the economic case for lithium-ion swap networks. All major swapping operators in India — Battery Smart, Indofast Energy, Yuma Energy, and Honda e:Swap — use lithium-ion battery architectures.

Lead-acid batteries retain a presence in the e-rickshaw segment, particularly in price-sensitive Tier-2 and Tier-3 markets where upfront cost remains the primary purchase criterion. However, their heavier weight, shorter cycle life, slower charge times, and environmental disposal challenges are driving a structural shift toward lithium-ion alternatives. Government incentives tied to advanced battery chemistries and operator preference for IoT-enabled smart batteries are accelerating lead-acid's displacement from organised swapping networks.

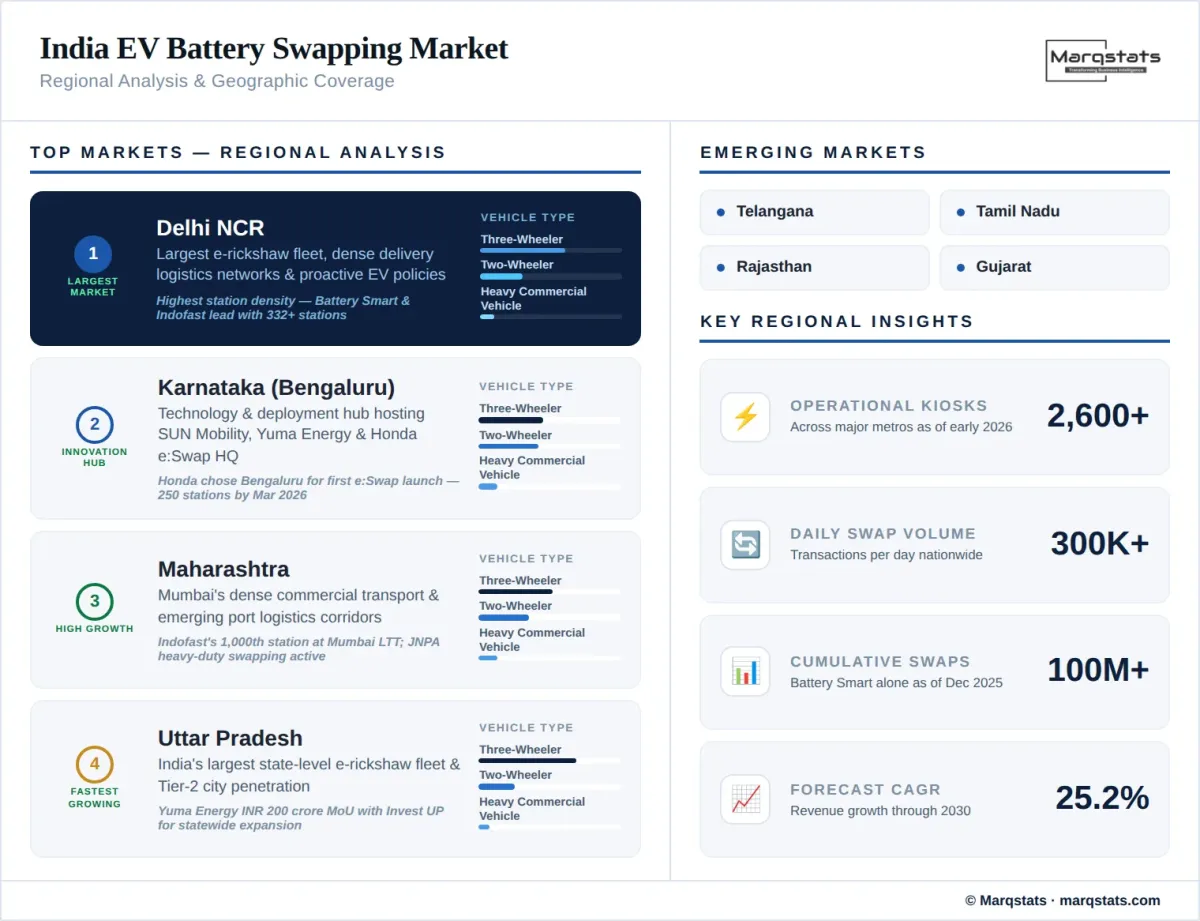

By Geography

Delhi NCR

Delhi NCR leads the India EV battery swapping market by station density and swap volume. The region benefits from a large e-rickshaw fleet, dense delivery logistics networks, and proactive state-level EV policies including Delhi's EV Policy 2020 which provided purchase incentives and charging infrastructure subsidies. Battery Smart and Indofast Energy both report their highest station concentrations in Delhi NCR, with Indofast operating 332 stations in the region as of September 2025. The territory's high population density and gig-economy activity create ideal utilisation dynamics for swap stations.

Karnataka (Bengaluru)

Bengaluru serves as the technology and deployment hub for India's battery swapping ecosystem. The city hosts the headquarters or major operations of SUN Mobility, Yuma Energy, and several swapping technology startups. Honda Power Pack Energy India chose Bengaluru as the first city for its e:Swap service launch in February 2025, deploying an initial 85 stations with plans for 250 by March 2026. Indofast Energy operates 259 stations in Bengaluru, making it the company's second-largest market. Karnataka's supportive EV policy ecosystem and strong technology talent pipeline reinforce the city's position as the innovation epicentre for swapping technology development.

Maharashtra (Mumbai–Pune Corridor)

Maharashtra represents a high-growth market anchored by Mumbai's dense commercial transport network and emerging logistics corridors. Indofast Energy commissioned its landmark 1,000th swap station at Mumbai's Lokmanya Tilak Terminus Railway Station in September 2025. The Indofast–Mumbai Metro Rail Corporation partnership to deploy 23 swap stations across the Aqua Line 3 corridor signals integration of swapping into mass transit infrastructure. Honda e:Swap plans 100 stations in Mumbai by March 2026. JNPA's heavy-duty swapping deployment at Nhava Sheva adds a port-logistics dimension to the state's swapping landscape.

Uttar Pradesh

Uttar Pradesh leads the India EV battery swapping market by state-level adoption according to industry analyses, driven by the country's largest e-rickshaw fleet and high last-mile demand in cities such as Lucknow, Varanasi, and Noida. Yuma Energy announced a plan to invest INR 200 crore in the state through an MoU with Invest UP to expand swapping infrastructure. The presence of swapping at locations like Banaras Railway Station signals penetration into Tier-2 urban nodes beyond metropolitan corridors.

Telangana and Andhra Pradesh

Hyderabad has emerged as a significant swapping market, with Indofast Energy operating 124 stations in the city as of September 2025. Telangana's state EV policy provides incentives for battery swapping station deployment, and the region's growing delivery logistics activity driven by its IT corridor creates sustained demand for commercial EV refuelling infrastructure.

How Competition Is Evolving

The India EV battery swapping market is moderately fragmented, characterised by a mix of well-funded startups, industry joint ventures, and OEM-backed entrants competing for station density, fleet partnerships, and geographic reach. Battery Smart holds the dominant market position, estimated to operate approximately 70% of India's organised battery-swapping infrastructure as of late 2025, with a cumulative 100 million swaps across its two-wheeler and three-wheeler network. The company has raised total funding of approximately USD 139 million, including a USD 21 million Series B round led by Rising Tide Energy in June 2025, with backing from Tiger Global Management, LeapFrog Investments, and the Asian Development Bank.

Indofast Energy, the 50:50 joint venture between IndianOil Corporation and SUN Mobility, has rapidly scaled to become the second-largest operator, commissioning its 1,000th station in September 2025 and targeting 2,750 stations supporting 150,000 vehicles by March 2026. The company's fuel-retail parentage through IndianOil provides access to existing energy distribution real estate, while SUN Mobility brings deep battery-swapping IP with over 160 intellectual property filings. Honda Power Pack Energy India's entry with 500 planned swap stations represents the first major global OEM commitment to India's swapping ecosystem, validating the market architecture for mass-volume two-wheeler applications. For insights into the broader electric bus market where swapping is gaining traction for intercity and fleet operations, see the India Electric Bus Market report on Marqstats.

Competitive strategies centre on network density in high-demand corridors, OEM partnerships for vehicle-swap compatibility, franchise models for capital-efficient scaling, and vertical integration across battery technology, station hardware, and fleet management software. The market's long-term competitive dynamics will be significantly influenced by the outcome of interoperability standardisation through BIS — operators building open, multi-OEM-compatible platforms are likely to achieve superior utilisation economics compared to closed, proprietary systems.

Companies Covered

The report profiles 16+ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the India EV battery swapping market covering the historical period 2021–2025 and forecast period 2026–2030, with 2025 as the base year. The study examines market size and revenue projections, growth trends, competitive landscape, segment-level forecasts by vehicle type, service model, and battery type, as well as regional analysis across India's major metropolitan and state-level markets.

Primary research includes assessment of operator milestones, OEM product launches, government policy developments, and infrastructure deployment patterns across leading battery swapping companies. Secondary research draws from government databases including NITI Aayog reports, Ministry of Power guidelines, PM E-DRIVE scheme documentation, industry body publications, company disclosures, regulatory filings, and trade media coverage. Market sizing employs bottom-up estimation validated against top-down industry benchmarks and operator-reported transaction volumes.