Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The vertical SaaS for construction management market encompasses cloud-based, subscription-licensed software platforms purpose-built for the construction industry’s unique workflows, compliance requirements, and multi-stakeholder coordination needs. The market scope covers project management and scheduling platforms, estimating and bid management tools, field collaboration and documentation software, BIM coordination platforms, financial management and accounting systems, resource and equipment management tools, safety and compliance solutions, and integrated construction ERP suites. The study period spans 2021–2030, with 2025 as the base year.

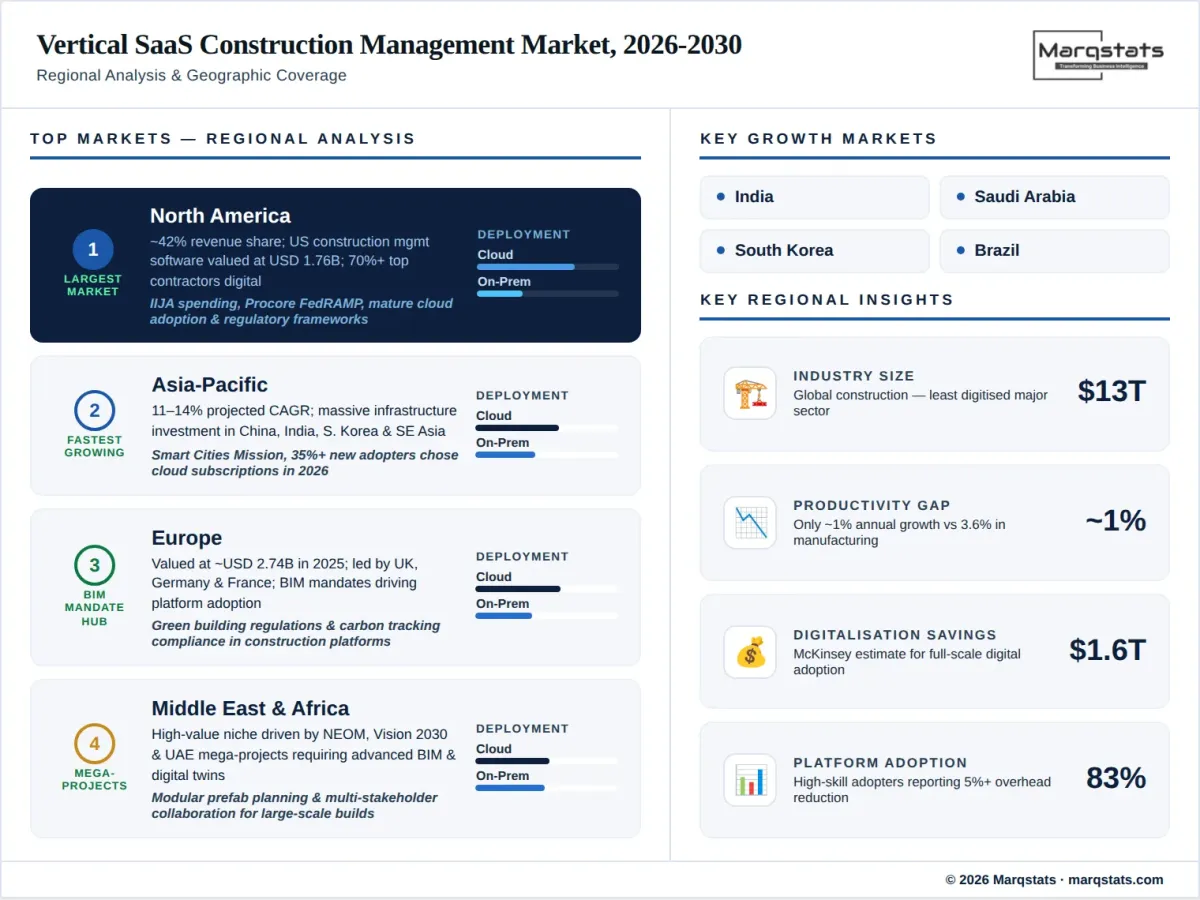

Construction is a USD 13 trillion global industry, yet it remains one of the least digitised sectors in the world economy. Labour productivity in construction has grown at only approximately 1% annually over the past two decades, compared with 2.8% for the total world economy and 3.6% for manufacturing. This productivity gap represents the core market opportunity for vertical SaaS platforms. McKinsey estimates that full-scale digitalisation of the construction industry could yield annual global savings of USD 1.6 trillion. Firms using integrated project management platforms have been shown to cut rework costs by up to 22% compared to traditional workflows, and by 2030, most major contractors worldwide are expected to use connected software suites linking design, fieldwork, and back-office operations into a single digital workflow.

The market is transitioning from single-point solutions toward integrated platform ecosystems. As of December 2025, 52% of Procore’s total annual recurring revenue was generated from customers using six or more products, illustrating the platform consolidation trend. Simultaneously, the industry is experiencing an inflection in AI adoption: Procore counts 66,000 unique active AI users and nearly 700 customers creating thousands of custom agents through its Agent Builder. Autodesk released digital twin features for live site updates in 2025, and Trimble launched Trimble One, an integrated project lifecycle solution connecting field sensors, GPS data, and cloud management systems. The convergence of BIM 6.0, AI, digital twins, IoT, and robotic field tools is creating a ‘digital construction’ paradigm that extends vertical SaaS platforms beyond project management into continuous asset lifecycle management.

Market Dynamics

Key Drivers

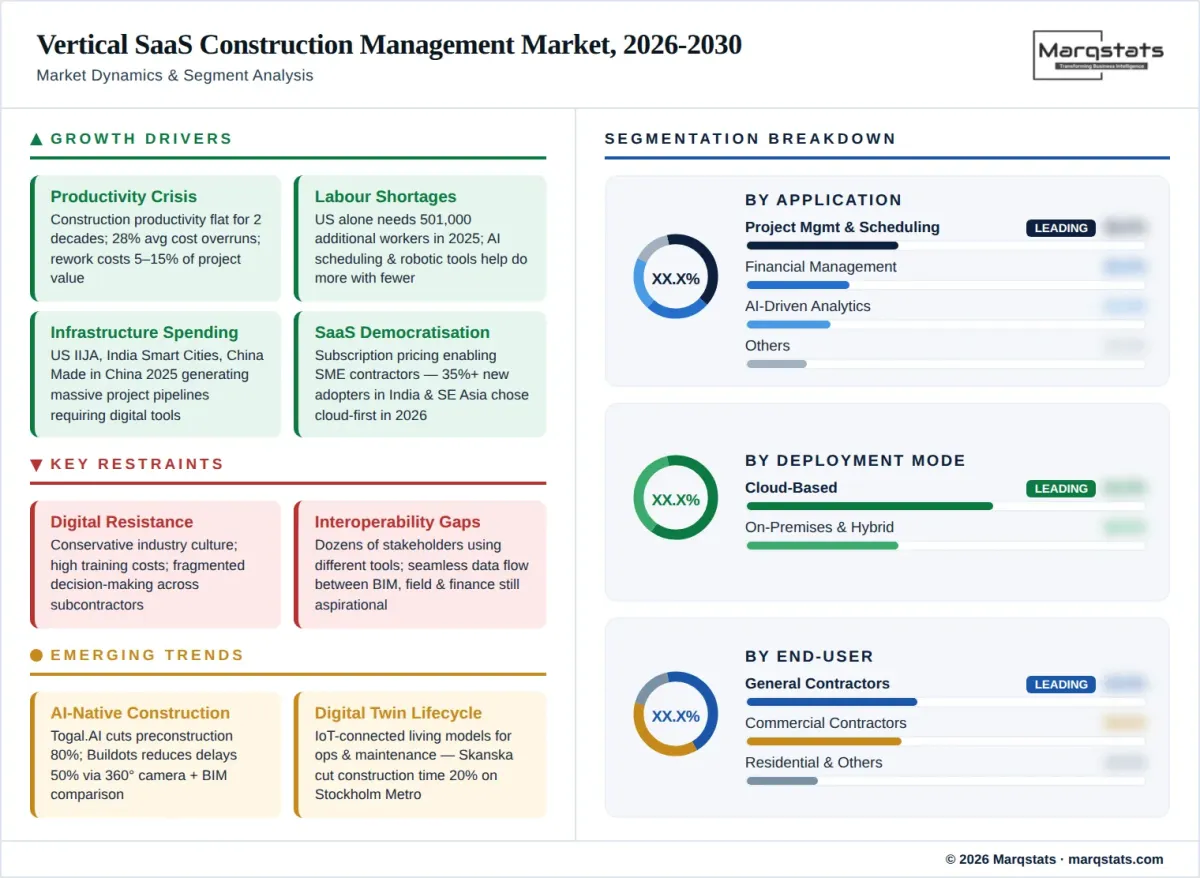

- Persistent construction productivity crisis: Construction productivity has stagnated for two decades while project complexity has increased. Cost overruns average 28% on large projects, and rework consumes 5–15% of project value. Vertical SaaS platforms directly address these inefficiencies through real-time visibility, automated workflows, and centralised data. Firms using integrated platforms report overhead reductions of 5%+ and profit margin improvements of four percentage points.

- Acute labour shortages accelerating automation demand: The global construction industry faces chronic workforce shortages, with the U.S. alone needing an estimated 501,000 additional workers in 2025. Vertical SaaS platforms with AI-driven scheduling, automated progress tracking, and robotic layout tools (such as Dusty Robotics’ FieldPrinter) enable firms to do more with fewer workers by eliminating manual processes and reducing coordination overhead.

- Government infrastructure investment driving project pipeline: Massive government spending programmes—including the U.S. Infrastructure Investment and Jobs Act, India’s Smart Cities Mission, and China’s Made in China 2025—are generating unprecedented project pipelines that require digital management tools. The U.S. Department of Transportation has issued Advanced Digital Construction Management Systems Grants specifically to promote software adoption.

- BIM mandates and green building compliance: Governments in the UK, Singapore, Scandinavia, and increasingly the U.S. are mandating BIM usage on public projects. California’s CALGreen amendments require large commercial projects to comply with whole-building lifecycle assessments, driving demand for software platforms that integrate carbon tracking, material specifications, and sustainability reporting with project management workflows.

- Subscription pricing democratising access for SME contractors: SaaS-based subscription models are replacing expensive on-premises software licences, enabling small and mid-sized contractors to access enterprise-grade tools. Over 35% of new adopters in India and Southeast Asia in 2026 chose cloud subscriptions as their first construction management platform, unlocking a massive underserved market segment.

Key Restraints

- Resistance to digital transformation in a conservative industry: Construction remains culturally resistant to technology adoption. High upfront training costs, reluctance to change long-standing paper-based procedures, and fragmented decision-making across subcontractors slow adoption. Many contractors still rely on spreadsheets, email, and phone calls for project coordination.

- Data interoperability and integration challenges: Construction projects involve dozens of stakeholders using different software tools. Despite growing adoption of open standards and APIs, achieving seamless data flow between design (BIM), field operations, financial systems, and equipment management remains a persistent challenge. True interoperability across the vendor ecosystem is still aspirational.

- Cybersecurity and data control concerns: Construction firms handling government contracts and sensitive infrastructure data face stringent security requirements. Procore’s achievement of FedRAMP Moderate Authorization in 2025 highlights the barrier—most vertical SaaS platforms lack equivalent certifications, limiting adoption in defence, critical infrastructure, and regulated public works projects.

- Internet connectivity limitations on remote construction sites: Cloud-based platforms require reliable internet connectivity, which is often unavailable on remote construction sites, highway projects, and rural infrastructure builds. While offline-capable mobile apps partially address this, the dependence on connectivity remains a practical constraint for cloud-first platforms.

Key Trends

- AI integration across the construction lifecycle: AI is becoming embedded at every stage—from automated takeoffs and cost estimation (Togal.AI reduces preconstruction time by up to 80%) to AI-powered site monitoring (Buildots uses 360° camera imagery to compare progress against BIM models, reducing delays by up to 50%) to predictive scheduling and risk forecasting. Procore’s acquisition of Datagrid in January 2026 signals the market’s pivot toward AI-native data connectivity and automated workflows like submittal reviews and RFI drafting.

- Digital twin adoption for infrastructure lifecycle management: The construction digital twin paradigm is moving beyond design-phase BIM into living, IoT-connected models that support operations and maintenance throughout an asset’s lifecycle. Trimble’s connected devices feed real-time data into digital twins, while Bentley Systems’ iTwin platform enables simulation and risk analysis in 4D construction models. Skanska’s use of digital twins on the Stockholm New Metro project cut construction time by 20%.

- Platform consolidation and the ‘super-app’ trend: Vendors are evolving from point solutions to integrated ecosystem platforms. Autodesk Construction Cloud bundles Autodesk Build, Autodesk Takeoff, and Autodesk Docs into a unified platform. Trimble launched Trimble One integrating field sensors, GPS, and cloud management. The industry is moving toward ‘super-apps’ where design, project tracking, equipment management, and sustainability reporting flow into a single interface.

- Drone, IoT, and robotics integration with SaaS platforms: Hardware-software convergence is accelerating. OpenSpace’s AI-powered 360° imagery integrates with Procore and BIM 360 for automated progress documentation. Dusty Robotics’ FieldPrinter syncs with BIM models for millimetre-precision floor layout. United Rentals and Procore announced a telematics integration in February 2026, syncing rented-equipment data into Procore Resource Management for unified asset tracking.

Market Segmentation

Project management and scheduling software leads the market with approximately 38% share in 2025, driven by universal demand for Gantt charts, cost tracking, RFIs (Requests for Information), and real-time dashboards. Real-time progress monitoring, automated reporting, mobile field access, and role-based permissions have made centralised project management platforms indispensable for both commercial and residential construction. Enhanced subcontractor coordination tools and automated issue tracking further strengthen this segment’s dominance.

AI-driven progress analytics is the fastest-growing application sub-segment at a projected 14.12% CAGR through 2031. These platforms use computer vision, machine learning, and IoT sensor data to automate progress tracking, predict delays, identify risk factors, and optimise resource allocation. Buildots, OpenSpace, and Disperse are among the leading AI analytics providers, while established players like Procore, Autodesk, and Oracle are embedding AI capabilities directly into their core platforms.

Financial management software is experiencing strong growth as construction firms prioritise cost control, budgeting precision, and compliance. Integration of invoicing, procurement, and payroll modules within unified construction platforms reduces financial risk and improves return on investment. Sage Group and Jonas Construction Software have historically dominated this segment, but cloud-native challengers are gaining share through integrated financial-operational platforms.

Cloud-based deployment dominates with approximately 62% market share in 2025, driven by scalability, lower upfront costs, rapid implementation, and real-time collaboration capabilities across distributed project teams. Public cloud platforms offered by AWS, Azure, and Google Cloud provide the infrastructure backbone. The shift accelerated during the pandemic when remote access became essential, and cloud adoption continues to climb as vendors link subscription pricing with mobile-first field applications.

On-premises solutions retain relevance in highly regulated defence, utility, and critical infrastructure projects where data control and localisation requirements mandate on-site hosting. Approximately 38% of the market still runs on-premises, though most large enterprises are piloting hybrid architectures where core financial data remains local while daily field documentation resides in the cloud. Trimble’s January 2025 tiered subscription bundles, linking hardware leasing with cloud-service entitlements, illustrate the hybrid migration path.

Commercial construction leads the end-user segments with approximately 39% share in 2025. The segment’s complexity—multi-phase projects involving office towers, retail complexes, and urban mixed-use developments—creates strong demand for digital oversight, tendering automation, subcontractor management, and client reporting. Higher project values and stringent compliance requirements make SaaS tool adoption economically compelling.

General contractors account for approximately 43% of demand, representing the broadest user base. These firms manage diverse project types and require end-to-end platforms covering pre-construction estimation through project closeout and warranty management. The shift toward integrated platforms is particularly pronounced among general contractors seeking to consolidate fragmented tool stacks.

Residential construction is the fastest-growing end-user segment, driven by increased housing demand and the rise of small-scale developers adopting digital tools for cost estimation, scheduling, and client communication. Buildertrend, founded in 2006, has become the leading platform for residential contractors, offering streamlined project management, financial tracking, and client-facing portals optimised for smaller-scale operations.

By Geography

North America

North America dominates the global market with approximately 42% revenue share in 2025, anchored by the United States where the construction management software market was valued at approximately USD 1.76 billion. The region benefits from mature regulatory frameworks, early cloud adoption, and large-scale infrastructure spending under the Infrastructure Investment and Jobs Act. Procore, headquartered in California, achieved FedRAMP Moderate Authorization in 2025, opening the federal government market. Over 70% of top U.S. contractors deploy digital management platforms. Canada is a secondary growth driver, with strong adoption among commercial and institutional builders.

Europe

Europe represents a significant market valued at approximately USD 2.74 billion in 2025, led by the UK, Germany, and France. The region’s growth is driven by BIM mandates on public projects (particularly in the UK and Scandinavia), stringent green building regulations, and increasing demand for sustainability compliance tracking within construction platforms. European firms are rolling out BIM plug-ins that track carbon footprint and waste diversion for net-zero buildings. Procore accelerated its EMEA expansion by launching in France and Germany, while niche players like Sablono (Berlin-based) address progress monitoring and quality management.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market at a projected CAGR of approximately 11–14%, driven by massive infrastructure investment in China, India, South Korea, and Southeast Asia. Government programmes such as India’s Smart Cities Mission and China’s urban development initiatives are generating enormous project pipelines. Over 35% of new platform adopters in India and Southeast Asia in 2026 chose cloud subscriptions, demonstrating strong receptivity to SaaS models. The region’s labour-intensive construction sector presents a particularly compelling case for automation and digital project management.

Middle East and Africa

The Middle East represents a high-value niche market, driven by mega-projects in Saudi Arabia (NEOM, Vision 2030), the UAE, and Qatar. These markets demand advanced BIM coordination, digital twin integration, and real-time multi-stakeholder collaboration across complex, large-scale infrastructure developments. Africa remains nascent but growing, with South Africa and Nigeria leading adoption among commercial contractors. Integrated digital twin platforms and modular prefabrication planning tools are gaining traction for mega-infrastructure developments across the region.

How Competition Is Evolving

The vertical SaaS for construction management market features a layered competitive structure. The top 10 companies account for approximately 65–68% of global market share, reflecting moderate concentration with meaningful room for niche players. Procore Technologies is the market leader with USD 1.32 billion in 2025 revenue, over 3 million projects running on its platform across 150+ countries, and 4,421 employees as of December 2025. The company’s platform-centric strategy—52% of ARR from customers using six or more products—positions it as the industry’s closest equivalent to a ‘system of record’ for construction management.

Autodesk, Oracle, and Trimble represent the enterprise tier, each bringing distinct strengths. Autodesk leverages its design software dominance (AutoCAD, Revit) to extend into construction management through Autodesk Construction Cloud. Oracle’s Primavera and Aconex platforms are deeply entrenched in large-scale infrastructure and government projects. Trimble’s differentiation lies in hardware-software integration, connecting field sensors, GPS devices, and robotic instruments with its cloud platform through Trimble One. Bentley Systems focuses on infrastructure digital twins via its iTwin and SYNCHRO platforms.

The mid-market segment is served by Sage Group (construction accounting and ERP), Buildertrend (residential-focused project management), Jonas Construction Software, and HCSS (heavy civil construction). A vibrant AI startup ecosystem is emerging: Buildots (360° AI site monitoring), OpenSpace (visual documentation), Togal.AI (automated estimating takeoffs), Dusty Robotics (robotic layout), and Disperse (AI progress analytics). Procore’s January 2026 acquisition of Datagrid—enhancing advanced reasoning, deep search, and multi-source data connectivity—signals the beginning of an M&A wave as incumbents acquire AI capabilities to maintain competitive positioning.

Companies Covered

The report profiles 16++ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the global vertical SaaS for construction management market covering the period 2021–2030, with 2025 as the base year, historical data from 2021 to 2025, and forecast projections from 2026 to 2030. The study examines market size in USD billion, growth trends, competitive landscape, and segment-level forecasts by application (project management, AI-driven analytics, financial management, resource management, safety and compliance), deployment mode (cloud, on-premises, hybrid), end-user (commercial contractors, general contractors, residential contractors, government and infrastructure agencies, owner-developers), and region.

The analysis covers the complete vendor ecosystem from integrated construction management platforms through specialised AI and IoT startups. Competitive profiling spans 16 companies with detailed analysis of product portfolios, revenue metrics, strategic partnerships, and M&A activity. The report provides strategic guidance on platform selection, digital transformation roadmaps, and ROI benchmarking for construction firms evaluating vertical SaaS adoption.